(Sponsored)

Things You Need to Know

- ESGold is Positioned for Immediate Cash Flow and Strong Returns: The Montauban Project in Quebec is set to generate near-term cash flow, offering a remarkable 142% IRR and less than a one-year payback period.

- ESGold’s Strategy Focuses on Sustainability and Innovation: The company’s unique approach transforms environmental liabilities into profitable assets by reprocessing historical tailings.

- Innovative Revenue Streams Enhance ESGold’s Market Position: ESGold is exploring groundbreaking ventures like producing green construction materials from tailings and utilizing mica in EV batteries, tapping into high-growth markets.

Thesis

ESGold represents a compelling investment at the nexus of environmental stewardship and financial returns. The Montauban Project in Quebec is poised to generate near-term cash flow by transforming contaminated tailings into valuable resources, including gold, silver, and mica. With exceptional economics—a 142% IRR and less than a one-year payback—ESGold maximizes profitability while addressing environmental remediation. Innovative ventures like green construction materials and mica for EV batteries expand its revenue streams, positioning the company as a leader in sustainable mining.

Backed by a scalable, replicable, and low-cost processing facility, and a strong leadership team, ESGold’s strategy focuses on self-financed exploration and disciplined growth. Government incentives and shareholder-aligned financing further enhance its value proposition. As the gold market remains robust, ESGold’s unique model offers investors a rare opportunity to capitalize on the synergy of sustainability, innovation, and profitability in a rapidly evolving mining industry.

Business Catalysts

- Immediate Revenue: With its Montauban plant set to begin operations imminently, ESGold is poised to generate organic cash flow by processing gold, silver, and mica from tailings. This positions the company for rapid payback and reinvestment into broader exploration.

- Exceptional Project Economics and ESG Alignment: The Montauban Project boasts an extraordinary IRR of 142% and a payback period of under one year, underpinned by low operational costs and government-backed environmental incentives.

- Project Replicability: The Montauban Project serves as a scalable blueprint for transforming orphaned mine sites into profitable, sustainable ventures, combining modern metallurgical advancements with environmental remediation. By demonstrating how legacy tailings can generate significant economic returns, ESGold is laying the groundwork for similar initiatives across the mining industry

Project Overview

The Montauban Project

- Location: 80 km west of Quebec City and 60 km northeast of Trois-Rivières

- Ownership: 100% ownership

- Land Claim 13,166 hectares

- Commodities: Gold, Silver, Mica

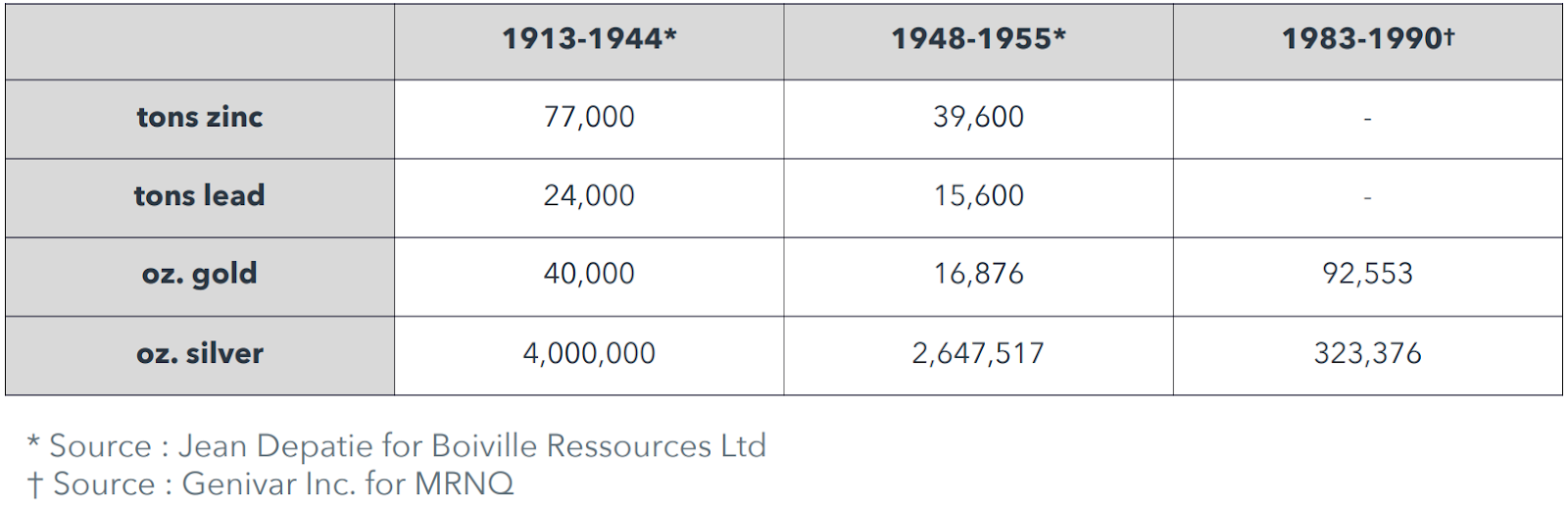

Montauban Historical Production

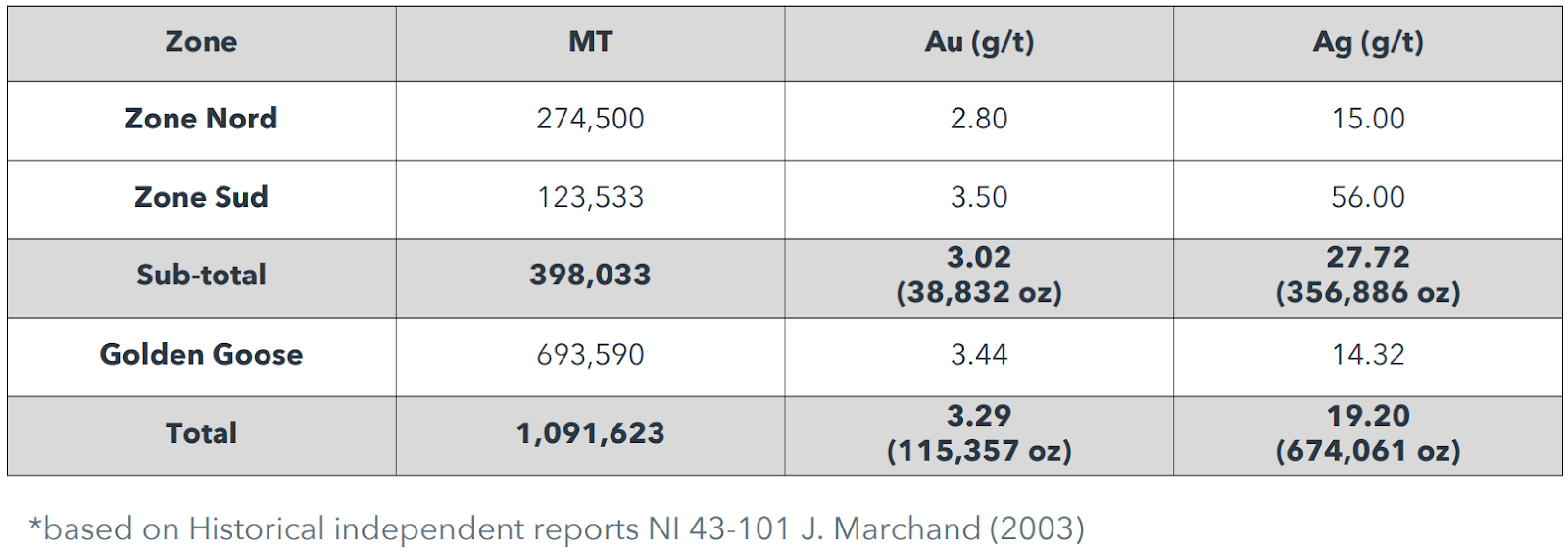

Near Surface Potential Resources

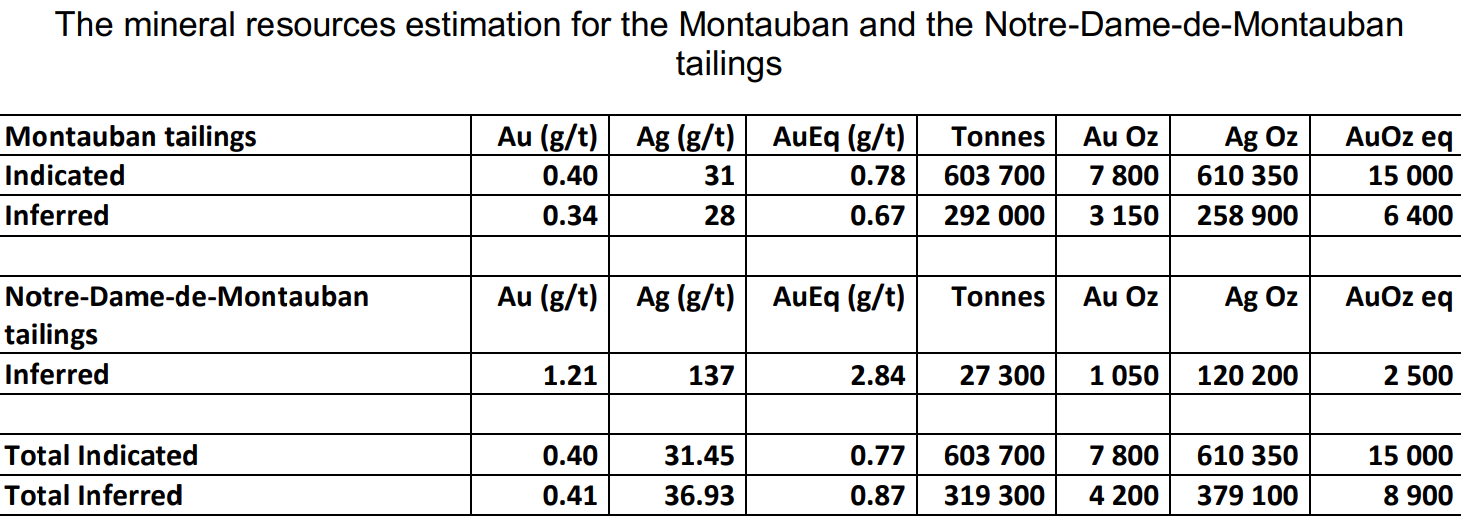

The Montauban Project is a pioneering initiative that is redefining modern mining by integrating sustainability, profitability, and environmental stewardship. Situated in Quebec’s highly mineralized region, this expansive 13,166-hectare land claim is rich in gold, silver, and base metals, with historical production exceeding $1.4 billion in value. ESGold’s primary focus is on reprocessing six historical tailings sites, including the Anacon Lead 1 site, turning decades-old environmental liabilities into lucrative opportunities. By using advanced milling technologies, the project not only recovers valuable resources such as gold, silver, and mica but also remediates the surrounding environment, restoring ecosystems that were previously impacted by legacy mining practices.

However, what truly sets ESGold and the Montauban apart is its replicability. The project is a pilot for innovative solutions that could be applied to orphaned mines worldwide, setting the stage for broader industry transformation. By integrating environmental stewardship with financial success, ESGold is proving that there are broader implications to its approach, creating major upside potential in the process.

Beyond that, the company is concentrating its efforts on the metallurgical optimization of gold and silver processing. ESGold is collaborating with four vendors to evaluate non-cyanide processing technologies, like bioleaching and reagent-based recovery, to evaluate recovery efficiency, environmental impact, and feasibility. Additionally, it is performing cyanide extraction tests to assess the integration of advanced milling technology. Together, the studies will determine an optimal solution, enhancing already impressive economics by improving recovery rates of precious metals in an environmentally conscious way.

With that said, the project’s financial projections are quite impressive at present. With a pre-tax IRR of 142%, a payback period of less than a year, and total projected revenues of C$111.5 million, Montauban demonstrates exceptional economic durability and profitability. ESGold’s scalable milling facility, permitted for up to 1,000 tonnes per day, requires only minor adjustments to begin tailings processing; the assembling of its processing circuit is expected to take roughly 6 to 9 months. This operational readiness ensures that ESGold can quickly capitalize on high mineral prices, generating significant revenue while laying the foundation for future exploration.

But it doesn’t stop there. Montauban’s exploration potential is equally compelling as its milling infrastructure. Despite its rich production history, the site has never undergone systematic exploration to map near-surface or deep mineralization. As a former producer within Canada’s renowned Volcanogenic Massive Sulfide (VMS) belt, it holds untapped opportunities for discovering high-grade deposits.

VMS deposits are highly valued for their depth and resource quality, and ESGold’s advanced drilling and modern exploration technologies will unlock this hidden potential. By self-funding through near-term cash flow, the company ensures long-term exploration success without unnecessary dilution, creating a sustainable cycle of growth and discovery.

Adding further credibility to the project is its President, Brad Kitchen, a key figure in Quebec’s mining success. Kitchen’s early work on the Windfall project—recently sold for C$2.16 billion—solidified his reputation for identifying high-value ventures. His involvement in the Montauban Project reflects a deep understanding of Quebec’s resource potential and a proven track record of working collaboratively with local stakeholders. This strategic leadership, combined with ESGold’s innovative approach to resource recovery, positions the Montauban Project as not only a regional leader but also a global exemplar of sustainable mining.

In all, Montauban exemplifies ESGold’s commitment to combining profitability with responsible mining. Through its multi-pronged strategy of metallurgical optimization, systematic exploration, and environmental remediation, the company is redefining the junior ming landscape. And given the replicability of its model, it offers a powerful blueprint for the industry’s evolution—proving that mining can be both economically robust and environmentally restorative.

Points of Criticism

- Dependence on Gold Prices: The project’s financial success is closely tied to rising gold prices, making it vulnerable to market fluctuations. A downturn in gold prices could negatively affect profitability and investor confidence.

- Unproven Diversification Efforts: Initiatives like producing green construction materials and exploring mica for EV batteries are speculative and lack proven market demand, posing risks to revenue generation.

- Execution Risks and Leadership Transition: Despite a strong new leadership team, ESGold must overcome challenges from past management and rebuild shareholder trust. The ambitious timeline for full production leaves little room for delays or setbacks.

Notable Updates in Q4 2024

- 11/26/2024: ESGold advancing the Montauban Project with a focus on sustainable mining practices by exploring non-cyanide processing technologies and collaborating with leading industry vendors to enhance environmental and economic outcomes. The company aims to reduce environmental impact, improve gold and silver recoveries, and lower operational costs, positioning itself as a leader in clean mining innovation while working towards production with strong financial metrics and community support.

- 11/12/2024: ESGold announced updated economic metrics for its Montauban Tailings Processing Project, highlighting an impressive internal rate of return (IRR) of 142% and a payback period of less than one year, with expected revenue of C$111.5 million. The project combines high profitability with environmental sustainability by processing historical tailings, generating cash flow, and contributing to regional environmental goals while positioning ESGold for long-term growth.

- 10/29/2024: ESGold launched an awareness campaign and is in discussions with financing partners to support the final construction of the Montauban Mine, targeting gold and silver production by Q2 2025. Additionally, the company applied for an OTCQB listing to increase visibility and market access, while exploring non-dilutive financing options to fund the project without reducing shareholder value.

- 10/15/2024: ESGold partnered with Caram Media Inc. and Senergy Communications Capital Inc. to enhance its visibility and strategic growth through targeted digital marketing and communications efforts. This collaboration aims to increase awareness of ESGold’s sustainable mining initiatives, particularly the Montauban project while fostering stronger relationships with shareholders and expanding the company’s market reach.

- 09/30/2024: ESGold closed a non-brokered private placement of 6,109,013 units, raising $610,901, with strong participation from existing and new strategic investors. The proceeds will support general administrative expenses and maintenance of the Montauban property in Quebec, as the company moves toward production.

Download

Disclosures

Analyst Certification

Each author of Maker Capital Research on this report certifies that (i) the recommendations and opinions expressed in this research accurately reflect the author’s personal, independent, and objective views about any of the designated securities discussed (ii) no part of the author’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the research, (iii) to the best of the author’s knowledge, she/he is not in receipt of material non-public information about the issuer, (iv) the author does not own common shares, options, or warrants in the company under coverage, and (v) the author adhere to the CFA Institute guidelines for analyst independence.

About Maker Capital Research

At Maker Capital Research, we are an independent equity research firm dedicated to uncovering high-quality businesses with market caps below $1 billion. Our expert team employs a fundamental, long-term investment strategy that emphasizes business sustainability and predictability. By meticulously analyzing a company’s operations, competitive advantages, financials, and management team, we assess the true quality of potential investments. Our research serves discerning investors who value in-depth insights and seek to make well-informed investment decisions. At Maker Capital Research, we provide the crucial information that empowers investors to identify and invest in promising businesses.

General Information

Maker Capital Research Corporation (MCR), a subsidiary of Apollo Relations, has created and distributed this report. This report is based on information we consider reliable; we have not been provided with any material non-public information by the company (or companies) discussed in this report. We do not represent that this report is accurate or complete and it should not be relied upon as such; further, any information in this report is subject to change without any formal or type of notice provided. Investors should consider this report as only one factor in their investment decisions; this report is not intended as a replacement for an investor’s independent judgment.

Apollo Relations is not an IIROC registered dealer and does not offer investment banking services to its clients. Apollo Relations (and its employees) do not own, trade, or have a beneficial interest in the securities of the companies we provide research services for and do not serve as an officer or Director of the companies discussed in this report. Apollo Relations does not make a market in any securities. This report is not disseminated in connection with any distribution of securities and is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Apollo Relations does not make any warranties, expressed or implied, as to the results to be obtained from using this information and makes no express or implied warranties for particular use. Anyone using this report assumes full responsibility for whatever results they obtain. This does not constitute a personal recommendation or take into account any financial or investment objectives, financial situations, or needs of individuals. This report has not been prepared for any particular individual or institution. Recipients should consider whether any information in this report is suitable for their particular circumstances and should seek professional advice. Past performance is not a guide for future results, future returns are not guaranteed, and loss of original capital may occur. Neither Apollo Relations nor any person employed by Apollo Relations accepts any liability whatsoever for any direct or indirect loss resulting from any use of its research or the information it contains.

This report contains “forward-looking” statements. Forward-looking statements regarding the Company and/or stock’s performance inherently involve risks and uncertainties that could cause actual results to differ from such forward-looking statements. Such statements involve a number of risks and uncertainties such as competition, technology shifts, market demand, and the company’s (and management’s) ability to correctly forecast financial estimates; please see the company’s MD&A “Risk Factors” Section for a more complete discussion of company-specific risks for the company discussed in this report.

Apollo Relations is receiving compensation in the form of 50,000 options from ESGold Corp for research coverage. Apollo Relations retains full editorial control over its research content. Apollo Relations does not have investment banking relationships and does not expect to receive any investment banking-driven income. Apollo Relations reports are primarily disseminated electronically and, in some cases, in printed form. Electronic reports are simultaneously available to all recipients in any form. Reprints of Apollo Relations reports are prohibited without permission. To receive future reports on covered companies please visit https://www.makercapitalresearch.com/research or subscribe to our website.

The information contained in this report is intended to be viewed only in jurisdictions where it may be legally viewed and is not intended for use by any person or entity in any jurisdiction where such use would be contrary to local regulations or which would require any registration requirement within such jurisdiction.

Copyright © 2024 Maker Capital Research, All rights reserved.