Things You Need to Know

- Delta Resources is exploring a highly prospective gold project in Thunder Bay, Ontario. The Delta-1 project is showcasing a remarkable high-grade gold deposit and significant expansion potential.

- The company’s strategic acquisitions have expanded its land package to 306 square kilometers, enhancing its exploration potential and attractiveness for acquisition.

- Recent strategic acquisitions, including the expansive Horne, Laurie, and Ternowesky properties, position Delta Resources to continue expanding its gold inventory while minimizing future financial commitments.

Thesis

Delta Resources presents a compelling investment opportunity in the Canadian gold exploration sector, distinguished by its strategic ownership of one highly prospective project. Its Delta-1 Gold Project near Thunder Bay, Ontario, is particularly noteworthy, with multiple drill intercepts revealing high-grade gold, including a remarkable 5.92 g/t Au over 31.0 meters. The company’s aggressive expansion and acquisition of adjacent properties highlights its commitment to maximizing the potential of this project, which now spans an impressive 306 square kilometers. Plus, the project’s proximity to critical infrastructure, including highways, power lines, and the port City of Thunder Bay, further enhances its value, positioning Delta Resources as a prime candidate for acquisition by larger mining firms looking to expand their portfolios with high-potential assets.

Business Catalysts

- High-Grade Gold at Delta-1: The promising drill results at Delta-1 underscore the project’s substantial resource potential. This discovery of high-grade gold positions Delta Resources for significant value appreciation as exploration continues.

- Large Land Claim with Critical Infrastructure at Delta-1: Delta-1’s expansive 306 square kilometer land package, strategically located near essential infrastructure, provides a robust foundation for future development and operational efficiency.

- Stronger Gold Prices: The ongoing global demand for gold creates a favorable market environment for Delta Resources. As gold prices remain strong, Delta’s potential gold deposits make it a highly attractive acquisition target poised to benefit from continued market momentum.

Project Overview

Delta-1

- Location: 50 km West of Thunder Bay, ON right on the TransCanada Highway 1.

- Ownership: 100% ownership

- History: Drilled 115 holes across 35,575 meters

- Commodities: Gold

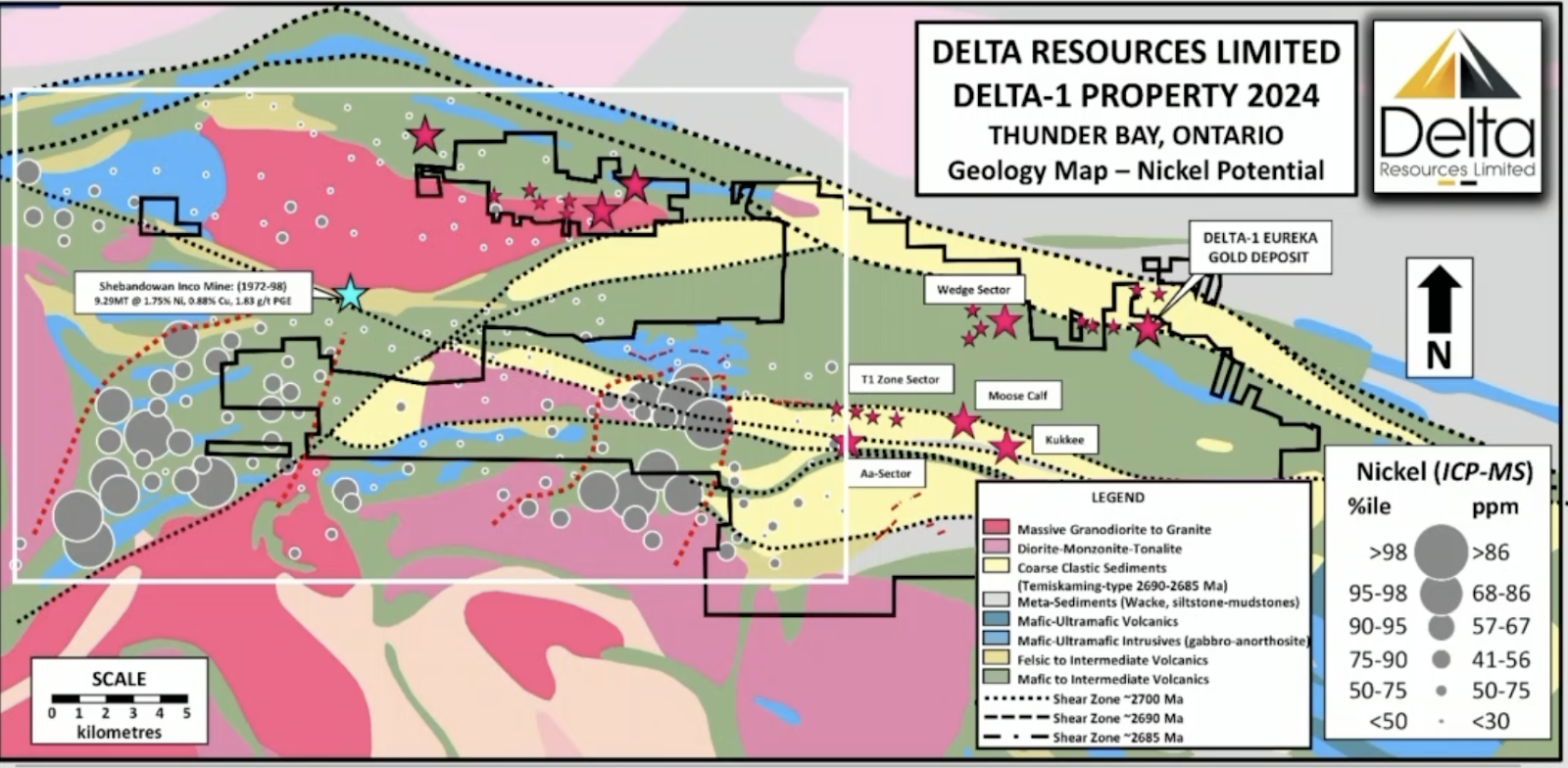

Delta-1 is Delta’s premier initiative, strategically positioned 50 kilometers west of Thunder Bay, Ontario, in the Shabandawan Greenstone Belt. This project is centered around a substantial gold inventory located at surface level, with the added advantage of being adjacent to the Trans-Canada highway. The gold mineralization extends impressively over a 2.5 km strike length, reaching from the surface down to a vertical depth of 300m. Notable drill results have revealed high-grade intercepts, including 5.92 g/t Au over 31m (with a highlight of 14.8 g/t Au over 11.9 m) and 1.79 g/t Au over 128.5m. The expansive property spans 306 square kilometers, where Delta has pinpointed several corridors of intense alteration and deformation. These corridors are aligned with and extend southward from the Eureka gold zone, offering significant untapped exploration potential.

With such a large land package and near surface-level drilling results, many of the bigger producers have been taking note of Delta. The reality right now is there is still more drilling to be done in and around the Delta-1 project, and the potential for higher-grade discoveries is high. The project’s location next to the Trans-Canada Highway, along with infrastructure, which includes several off-highway logging roads shelter, and a communication tower, east of the property, is paramount to any exploration company looking to turn their project into a future potential mine producing site.

At the end of 2023, Delta had completed approximately 25,000 meters of drilling to estimate the gold resources in the area. While this is not yet a 43-101 compliant resource, the zone extended over 2 km of strike length with a surface-to-vertical depth of 250 meters. Subsequently, the company expanded its efforts to the east, in 2024, with an additional 10,000 meters of drilling, extending the strike by approximately 500 meters in length and 50 meters in depth. To date, Delta has completed 35,575 meters of drilling over 115 holes.

See the drilling results from Delta-1 below:

Going into Q4 2024/Q1 2025, Delta-1 continues to be the number one focus for Delta Resources. All future exploration work will be centered around the current land package (see map below). The fault-bounded sedimentary basins on the newly acquired land packages appear to have an identical geological setting as the Eureka discovery zone giving its management team the conviction that there is a significant amount of gold to the South and West of Eureka.

Delta remains focused on gold exploration at Delta-1 but, the western portion of the property has excellent polymetallic copper-nickel potential. In 1999, the Geological Survey of Ontario completed a till survey, focused on the glacial dispersion trails whereby they outlined a dispersion trail pointing to the old Inco Mine (see the blue star to the West in the map below) and to an untested target sitting on the Delta-1 property.

Points of Criticism

- Capital Constraints Limit The Size of Drilling Campaigns: With $2.34 million cash on its balance sheet, Delta Resources’ capital constraints may limit the amount of drilling the company can accomplish in the near term. Drill campaigns are capital-intensive thus requiring ample funds to run a large-scale program.

- Possible Shareholder Dilution: The company’s reliance on external funding, given its inability to generate cash flow, highlights the need for continuous capital raises or asset sales to maintain operational momentum and support ongoing exploration activities. The company may need to raise capital from the market.

- Exploration Project is Not Fully De-Risked: Delta is currently in the exploration stage of the Lassonde curve and is still missing some of the pieces for it to be a de-risked project. Much of the recent discovery has not been put through a pre-feasibility study nor is there a PEA (preliminary economic assessment), so the true economic value of a potential deposit has not yet been determined. In addition, the resource is not 43-101 compliant yet.

Notable Updates in Q3 2024

- 08/26/2024: Delta Resources reached an agreement to acquire a 100% interest in the Horne and Laurie properties at its Delta-1 project by issuing shares and warrants, thereby eliminating $1.35 million in future cash payments and work commitments. This strategic acquisition enhances Delta’s flexibility and positions it to continue expanding its gold inventory while exploring its extensive land package in the Shebandowan Belt.

- 08/06/2024: Delta Resources acquired a 100% interest in the Ternowesky property, expanding its land position in the Shebandowan Greenstone Belt to over 306 square kilometers. This strategic acquisition strengthens Delta’s potential for discovering multiple gold and magmatic copper deposits, with plans for further exploration in 2024.

- 07/09/2024: Delta Resources completed an extensive till sampling program at its Delta-1 Gold Project, covering 80 km² with 224 sample sites to expand on previous successful surveys. The results, expected later this summer, will guide further exploration, building on the discovery of the Eureka Gold Zone and exploring the broader potential of the Shebandowan area.

- 06/27/2024: Delta Resources reported final assay results from its 2024 drilling program at the Delta-1 Gold project, which confirmed the internal continuity of the Eureka Zone and extended the mineralized zone to a vertical depth of 300 meters. Significant high-grade intersections were reported, and the results will guide the next drilling campaign, with further exploration ongoing across the expanded 220-square-kilometer property.

Download

Disclosures

Analyst Certification

Each author of Maker Capital Research on this report certifies that (i) the recommendations and opinions expressed in this research accurately reflect the author’s personal, independent, and objective views about any of the designated securities discussed (ii) no part of the author’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the research, (iii) to the best of the author’s knowledge, she/he is not in receipt of material non-public information about the issuer, (iv) the author does not own common shares, options, or warrants in the company under coverage, and (v) the author adhere to the CFA Institute guidelines for analyst independence.

About Maker Capital Research

At Maker Capital Research, we are an independent equity research firm dedicated to uncovering high-quality businesses with market caps below $1 billion. Our expert team employs a fundamental, long-term investment strategy that emphasizes business sustainability and predictability. By meticulously analyzing a company’s operations, competitive advantages, financials, and management team, we assess the true quality of potential investments. Our research serves discerning investors who value in-depth insights and seek to make well-informed investment decisions. At Maker Capital Research, we provide the crucial information that empowers investors to identify and invest in promising businesses.

General Information

Maker Capital Research Corporation (MCR), a subsidiary of Apollo Relations, has created and distributed this report. This report is based on information we consider reliable; we have not been provided with any material non-public information by the company (or companies) discussed in this report. We do not represent that this report is accurate or complete and it should not be relied upon as such; further, any information in this report is subject to change without any formal or type of notice provided. Investors should consider this report as only one factor in their investment decisions; this report is not intended as a replacement for an investor’s independent judgment.

Apollo Relations is not an IIROC registered dealer and does not offer investment banking services to its clients. Apollo Relations (and its employees) do not own, trade, or have a beneficial interest in the securities of the companies we provide research services for and do not serve as an officer or Director of the companies discussed in this report. Apollo Relations does not make a market in any securities. This report is not disseminated in connection with any distribution of securities and is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Apollo Relations does not make any warranties, expressed or implied, as to the results to be obtained from using this information and makes no express or implied warranties for particular use. Anyone using this report assumes full responsibility for whatever results they obtain. This does not constitute a personal recommendation or take into account any financial or investment objectives, financial situations, or needs of individuals. This report has not been prepared for any particular individual or institution. Recipients should consider whether any information in this report is suitable for their particular circumstances and should seek professional advice. Past performance is not a guide for future results, future returns are not guaranteed, and loss of original capital may occur. Neither Apollo Relations nor any person employed by Apollo Relations accepts any liability whatsoever for any direct or indirect loss resulting from any use of its research or the information it contains.

This report contains “forward-looking” statements. Forward-looking statements regarding the Company and/or stock’s performance inherently involve risks and uncertainties that could cause actual results to differ from such forward-looking statements. Such statements involve a number of risks and uncertainties such as competition, technology shifts, market demand, and the company’s (and management’s) ability to correctly forecast financial estimates; please see the company’s MD&A “Risk Factors” Section for a more complete discussion of company-specific risks for the company discussed in this report.

Apollo Relations is receiving cash compensation from Delta Resources for 6-months of research coverage. Apollo Relations retains full editorial control over its research content. Apollo Relations does not have investment banking relationships and does not expect to receive any investment banking-driven income. Apollo Relations reports are primarily disseminated electronically and, in some cases, in printed form. Electronic reports are simultaneously available to all recipients in any form. Reprints of Apollo Relations reports are prohibited without permission. To receive future reports on covered companies please visit https://www.makercapitalresearch.com/research or subscribe to our website.

The information contained in this report is intended to be viewed only in jurisdictions where it may be legally viewed and is not intended for use by any person or entity in any jurisdiction where such use would be contrary to local regulations or which would require any registration requirement within such jurisdiction.

Copyright © 2024 Maker Capital Research, All rights reserved.